Predictive Models - Regression

Linear Regression

Least squares minimizes the sum of squared errors

This is the same as maximizing the likelihood of observed data if you start thinking of the problem in terms of probabilities and probability distribution functions

Sometimes called “maximum likelihood estimation”

import numpy as np

import matplotlib.pyplot as plt

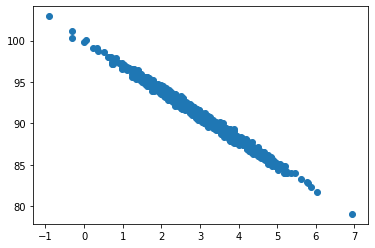

pageSpeed = np.random.normal(3.0, 1.0, 1000)

purchaseAmount = 100 - (pageSpeed + np.random.normal(0, 0.1, 1000)) * 3

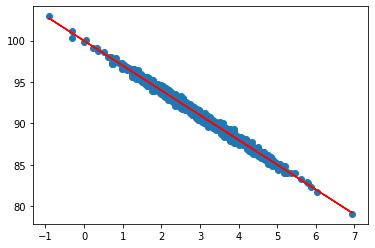

plt.scatter(pageSpeed, purchaseAmount)

plt.show()

from scipy import stats

slope, intercept, r_value, p_value, std_err = stats.linregress(pageSpeed, purchaseAmount)

R squared value shows a really good fit

r_value ** 2

0.9902693736994506

def predict(x):

return slope * x + intercept

fitline = predict(pageSpeed)

plt.scatter(pageSpeed, purchaseAmount)

plt.plot(pageSpeed, fitline, c="r")

plt.show()

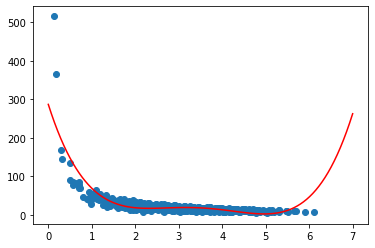

Polynomial Regression

np.random.seed(2020)

pageSpeed = np.random.normal(3.0, 1.0, 1000)

purchaseAmount = np.random.normal(50.0, 10.0, 1000) / pageSpeed

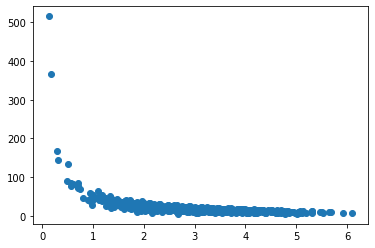

plt.scatter(pageSpeed, purchaseAmount)

plt.show()

x = np.array(pageSpeed)

y = np.array(purchaseAmount)

p4 = np.poly1d(np.polyfit(x, y, 4))

p4

poly1d([ 2.43355681, -33.88400278, 168.02869346, -354.05850288,

286.61089763])

xp = np.linspace(0, 7, 100)

plt.scatter(x, y)

plt.plot(xp, p4(xp), c="r")

plt.show()

from sklearn.metrics import r2_score

r2 = r2_score(y, p4(x))

r2

0.6980067595161712

Multiple regression

import pandas as pd

df = pd.read_excel("http://cdn.sundog-soft.com/Udemy/DataScience/cars.xls")

df.head()

| Price | Mileage | Make | Model | Trim | Type | Cylinder | Liter | Doors | Cruise | Sound | Leather | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 17314.103129 | 8221 | Buick | Century | Sedan 4D | Sedan | 6 | 3.1 | 4 | 1 | 1 | 1 |

| 1 | 17542.036083 | 9135 | Buick | Century | Sedan 4D | Sedan | 6 | 3.1 | 4 | 1 | 1 | 0 |

| 2 | 16218.847862 | 13196 | Buick | Century | Sedan 4D | Sedan | 6 | 3.1 | 4 | 1 | 1 | 0 |

| 3 | 16336.913140 | 16342 | Buick | Century | Sedan 4D | Sedan | 6 | 3.1 | 4 | 1 | 0 | 0 |

| 4 | 16339.170324 | 19832 | Buick | Century | Sedan 4D | Sedan | 6 | 3.1 | 4 | 1 | 0 | 1 |

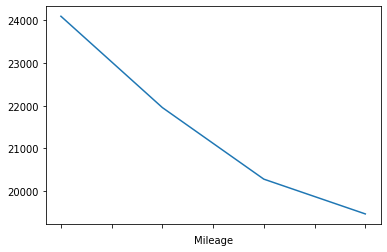

df1 = df[["Mileage", "Price"]]

bins = np.arange(0, 50000, 10000)

groups = df1.groupby(pd.cut(df1["Mileage"], bins)).mean()

groups.head()

| Mileage | Price | |

|---|---|---|

| Mileage | ||

| (0, 10000] | 5588.629630 | 24096.714451 |

| (10000, 20000] | 15898.496183 | 21955.979607 |

| (20000, 30000] | 24114.407104 | 20278.606252 |

| (30000, 40000] | 33610.338710 | 19463.670267 |

groups["Price"].plot.line()

<matplotlib.axes._subplots.AxesSubplot at 0x292b9325488>

import statsmodels.api as sm

from sklearn.preprocessing import StandardScaler

scale = StandardScaler()

X = df[["Mileage", "Cylinder", "Doors"]]

y = df["Price"]

X[["Mileage", "Cylinder", "Doors"]] = scale.fit_transform(

X[["Mileage", "Cylinder", "Doors"]])

R:\Work\Anacond\lib\site-packages\ipykernel_launcher.py:2: SettingWithCopyWarning:

A value is trying to be set on a copy of a slice from a DataFrame.

Try using .loc[row_indexer,col_indexer] = value instead

See the caveats in the documentation: https://pandas.pydata.org/pandas-docs/stable/user_guide/indexing.html#returning-a-view-versus-a-copy

R:\Work\Anacond\lib\site-packages\pandas\core\indexing.py:965: SettingWithCopyWarning:

A value is trying to be set on a copy of a slice from a DataFrame.

Try using .loc[row_indexer,col_indexer] = value instead

See the caveats in the documentation: https://pandas.pydata.org/pandas-docs/stable/user_guide/indexing.html#returning-a-view-versus-a-copy

self.obj[item] = s

X

| Mileage | Cylinder | Doors | |

|---|---|---|---|

| 0 | -1.417485 | 0.52741 | 0.556279 |

| 1 | -1.305902 | 0.52741 | 0.556279 |

| 2 | -0.810128 | 0.52741 | 0.556279 |

| 3 | -0.426058 | 0.52741 | 0.556279 |

| 4 | 0.000008 | 0.52741 | 0.556279 |

| ... | ... | ... | ... |

| 799 | -0.439853 | 0.52741 | 0.556279 |

| 800 | -0.089966 | 0.52741 | 0.556279 |

| 801 | 0.079605 | 0.52741 | 0.556279 |

| 802 | 0.750446 | 0.52741 | 0.556279 |

| 803 | 1.932565 | 0.52741 | 0.556279 |

804 rows × 3 columns

est = sm.OLS(y, X).fit()

est.summary()

| Dep. Variable: | Price | R-squared (uncentered): | 0.064 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared (uncentered): | 0.060 |

| Method: | Least Squares | F-statistic: | 18.11 |

| Date: | Wed, 28 Oct 2020 | Prob (F-statistic): | 2.23e-11 |

| Time: | 14:40:09 | Log-Likelihood: | -9207.1 |

| No. Observations: | 804 | AIC: | 1.842e+04 |

| Df Residuals: | 801 | BIC: | 1.843e+04 |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Mileage | -1272.3412 | 804.623 | -1.581 | 0.114 | -2851.759 | 307.077 |

| Cylinder | 5587.4472 | 804.509 | 6.945 | 0.000 | 4008.252 | 7166.642 |

| Doors | -1404.5513 | 804.275 | -1.746 | 0.081 | -2983.288 | 174.185 |

| Omnibus: | 157.913 | Durbin-Watson: | 0.008 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 257.529 |

| Skew: | 1.278 | Prob(JB): | 1.20e-56 |

| Kurtosis: | 4.074 | Cond. No. | 1.03 |

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

y.groupby(df.Doors).mean()

Doors

2 23807.135520

4 20580.670749

Name: Price, dtype: float64

Surprisingly more doors doesn’t mean higher price.

So it’s pretty useless as a predictor here.

scaled = scale.transform([[45000, 8, 4]])

predicted = est.predict(scaled[0])

scaled, predicted

(array([[3.07256589, 1.96971667, 0.55627894]]), array([6315.01330583]))

Multi-Level Models